By

By

In recent years punitive tax rules, changes to stamp duty and other measures designed to make life challenging for small landlords have been introduced by successive Conservative governments.

These changes principally affect the way buy-to-let (BtL) property is taxed. Coupled with the rapid rise in interest rates, many people are talking about the death of BtL in the UK and an exodus of landlords.

So does BtL no longer stack up? In this post I am taking a deep dive into the numbers to examine the reality.

Section 24

It is true that the combination of Section 24 and higher interest rates, have essentially put most buy-to-let investments under water. To demonstrate, I have set out the impact of higher interest rates and section 24 on a property currently for sale on our MyPropTech.com platform.

The property is a one bedroom apartment built by a national housebuilder in a London commuter town, brief details are set out below.

- 1 Bedroom Apartment

- Area = 429 ft²

- Retail Asking Price = £232,000

- Estimated Rental = £14,400 p.a.

- Service Charge = £2.25 per ft²a.

Purchased by UK Based Investor

If the property, were to be purchased by a UK based property investor who is a higher rate tax-payer, the investment would look as follows:

- Purchase Price - £232,000

- Stamp Duty - £6,960

- Deposit - £58,000 (25%)

- Interest Rate – 5.87% interest only

- Total Cash Required - £64,960

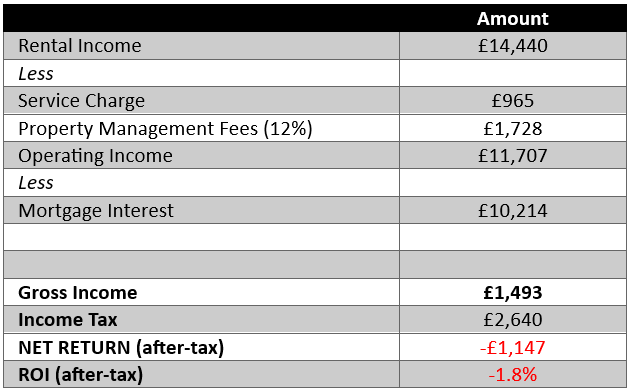

In this scenario, the investor’s return in the first year would be as follows:

Based on this scenario, the investor would spend £64,960 to purchase the property and although their gross income would be positive (£1,493) after the impact of income tax (which is charged on turnover rather than profit) the investors return would be -£1,147 p.a.

Hardly a ringing endorsement for BtL, so BtL must be dead right? Maybe not. Let’s look at what the impact would be if the same property was purchased within a company structure.

Purchased in a company by a UK investor

If the same purchaser purchased the property in a company rather than their own name, they would have the advantage of being able to offset 100% of their mortgage interest. Assuming they already own their own home the stamp duty position would be the same: a 3% surcharge applies to either company or second home purchase.

However, I am assuming that the same buyer would be subject to a higher interest rate (6.56%) as well as a higher deposit of 35%. So, in this case the scenario would change to:

- Purchase Price - £232,000

- Stamp Duty - £6,960

- Deposit - £81,200 (35%)

- Interest Rate – 6.56% interest only

- Total Cash Required - £88,160

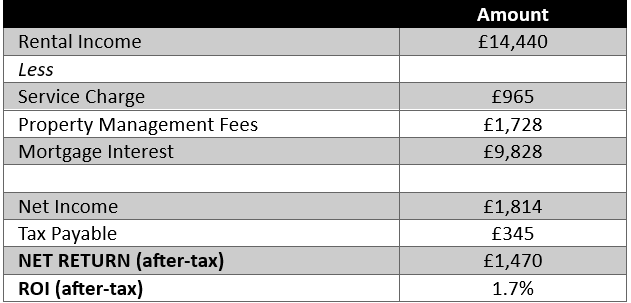

In this scenario, the investors return in the first year would be as follows:

Based on this scenario, the investor would spend £88,160 to purchase the property and the net income after tax to the company would be £1,470 providing a ROI (after corporation tax) of 1.7%. The investor would still be liable for income tax on any dividends they paid to themselves.

Introducing MyPropTech Dynamic Pricing™

The MyPropTech platform has price setting mechanism which aggregates purchasers into groups of 10 in the same development, assuming 10 buyers all agree to purchase 10 different properties they will be discounted.

In this scenario this apartment is available to purchase at a 10% discount (as part on an aggregated transaction using MyPropTech Dynamic Pricing™)

So now the scenario, will be as follows:

- Purchase Price - £208,000

- Stamp Duty - £6,264

- Deposit - £73,080 (35%)

- Interest Rate – 6.56% interest only

- Total Cash Required - £79,344

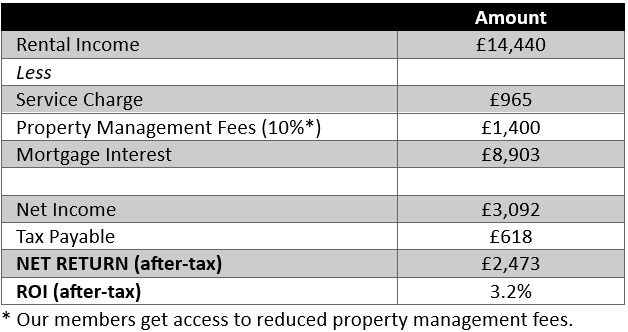

In this scenario, the investors return in the first year would be as follows:

Based on this scenario, the investor would spend £79,344 to purchase the property and their net income would be £2,473 providing a ROI (after corporation tax) of 3.2%.

Alternative Investments

Many people will look at this will say is, but I can invest the same capital in X [lets, call it Money Market] account which will provide a guaranteed return of 5%. Plus, I don’t need to worry about tenants and other risks, etc. Why would I invest in property when I can buy this amazing investment with ‘no risk’?

Well, the reality is these investments don’t come with no risk, they come with OPPORTUNITY COST. People who say this ignore the very reason why people invest in property in the first place, for potential capital and income growth over time.

So, let’s consider the same investment over time making the following assumptions.

- Average Inflation – 2.0% p.a.

- Rental Growth – 5% p.a.

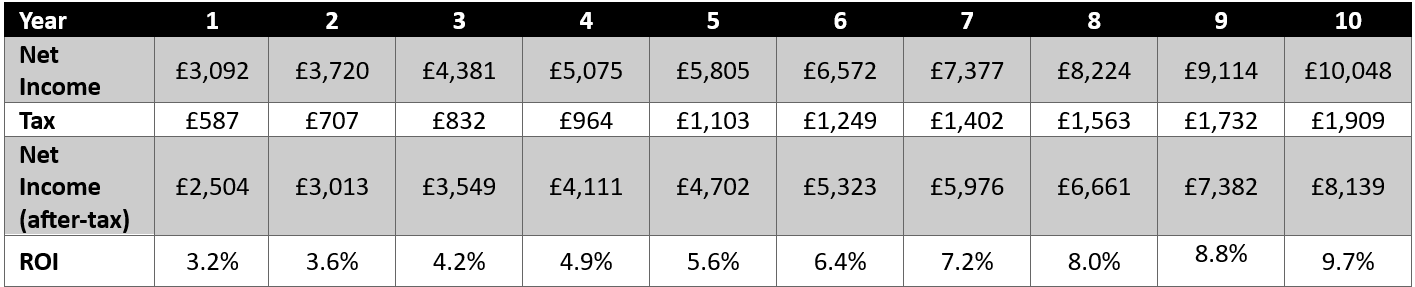

Purely from a Return on Investment (ROI) perspective, the investment will ultimately out perform a straight forward investment in a Money Market account at say 5% p.a.

So, let’s compare investing the same £79,344 at a straightforward fixed account returning 5% p.a.

Comparing the two investments, the property will be out performed by a simple cash account for the first three years and then will fall rapidly behind the return of a property.

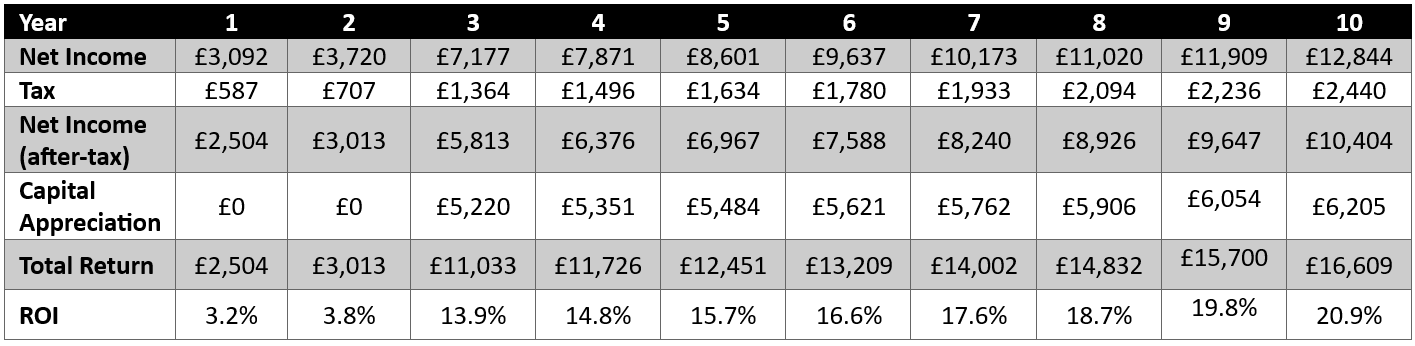

Capital Appreciation

However, this simple comparison doesn’t consider any capital appreciation over time. So let re-run the same numbers assuming the following, from year 3:

- Investor can re-finance the property at an interest only mortgage at 4.5%

- Capital appreciation annually of 2.5%

The numbers now start to show the long-term power of property investment.

Now let’s compare total returns to our Money Market account.

Now the real estate investment significantly out performs the Money Market investment. And, this is in a scenario where I have been very conservative with rental and capital appreciation.

Buy-to-Let Isn’t Dead, Investors Need to Change

The reality is that Buy-to-Let is not dead, investors will simply need to change. Investors will need to be far more sophisticated in the way they approach investment decisions. Simply buying and property renting it out and hoping for the best won’t work. Investors will need to analyse investments in a much more considered way to determine whether or not they are viable, before rushing in.

Our expectation is that the market will see the following changes over the coming years:

- Most investors will buy in a company structure

- Investors will focus on new build where aggregated discounts can be generated to make investments stack up

- Developers will discount properties to sell through them

- International investors will return to the UK, where they have the benefit of better income tax rates as well as the benefit of a weaker pound sterling.